From Static Policies to Autonomous Insurance: How AI enables Real-Time Coverage

Adapting insurance coverage to user needs in real time using contextual and behavioral analytics

- How embedded insurance delivers protection at the moment of need, integrating coverage directly into digital experiences and evolving from static policies to just-in-time and eventually to autonomous insurance models.

- How behavioral analytics and real-time data streams enable dynamic pricing and personalized coverage, using signals from devices, transactions, and geospatial data to assess risk continuously for different insurance personas such as underwriters, innovation product leads, marketing managers, etc.

- How a governed Lakehouse data foundation powers autonomous insurance, unifying data, AI, and analytics to enable adaptive policies, faster product innovation, and improved underwriting outcomes.

Insurance was designed for a slower world. Policies were priced once a year, risk was assessed periodically, and coverage changed only after major life events. But today, risk moves faster than policy cycles. A driver’s behavior can change over time, a digital transaction can trigger fraud in seconds, and a traveler’s exposure to risk can shift between booking a ticket and boarding the plane. Yet most insurance products still operate as if risk were static.

Imagine buying insurance the same way you activate navigation in a ride-sharing app, instantly, contextually, and only for the time you need it.

You get to the airport and activate flight coverage.

You start a road trip, and your auto policy adjusts to the risk of that journey.

You initiate a high-value digital transaction, and temporary cyber protection auto-activates.

This is the promise of embedded insurance: protection delivered precisely at the moment of need, integrated seamlessly into the digital experiences consumers already trust. What began as a distribution innovation is quickly becoming much more, a transformation in how insurance products are designed, priced, and delivered.

What Is Embedded Insurance?

Embedded insurance is a new model that is emerging to close the gap. It refers to additional coverage protection offered at the customer point of usage or sale, creating a sense of trust by associating offers with activities that consumers already engage in, from companies they trust. It promises contextual, real-time protection (per trip, per asset, per behavior).

Embedded insurance is coverage integrated directly into the digital experiences people already use providing protection at the exact moment of need. It converges naturally with Usage-Based Insurance (UBI), where premiums are determined by real-time behavior rather than static risk profiles. Together, they enable coverage that is contextual, dynamically priced, and tailored to the individual. As noted in the Databrick’s Insurance market outlook, ‘From Proxies to Observed Behavior’ is the shift at scale in modern data platforms that facilitates this trend. This convergence represents more than a new distribution channel- it marks the evolution of insurance itself, from static annual policies to just-in-time coverage, and ultimately to autonomous insurance systems that continuously adapt to risk.

Consumers still value human advice, so the physical agent’s role remains critical. What changes is scale: AI enables 24/7 advisory support, equipping agents with behavioral insights, risk context, and personalized recommendations in real time. APIs make coverage portable across channels, mobile apps, checkout pages, call centers, partner platforms, and meeting customers wherever they are.

Market growth reflects the momentum behind this model. According to marketresearch.com, embedded insurance is projected to grow at roughly 25-30% CAGR through 2030, potentially reaching $500B in premiums. For insurers, distributors, and digital platforms, this represents both a new distribution channel and a pathway toward data-driven risk intelligence.

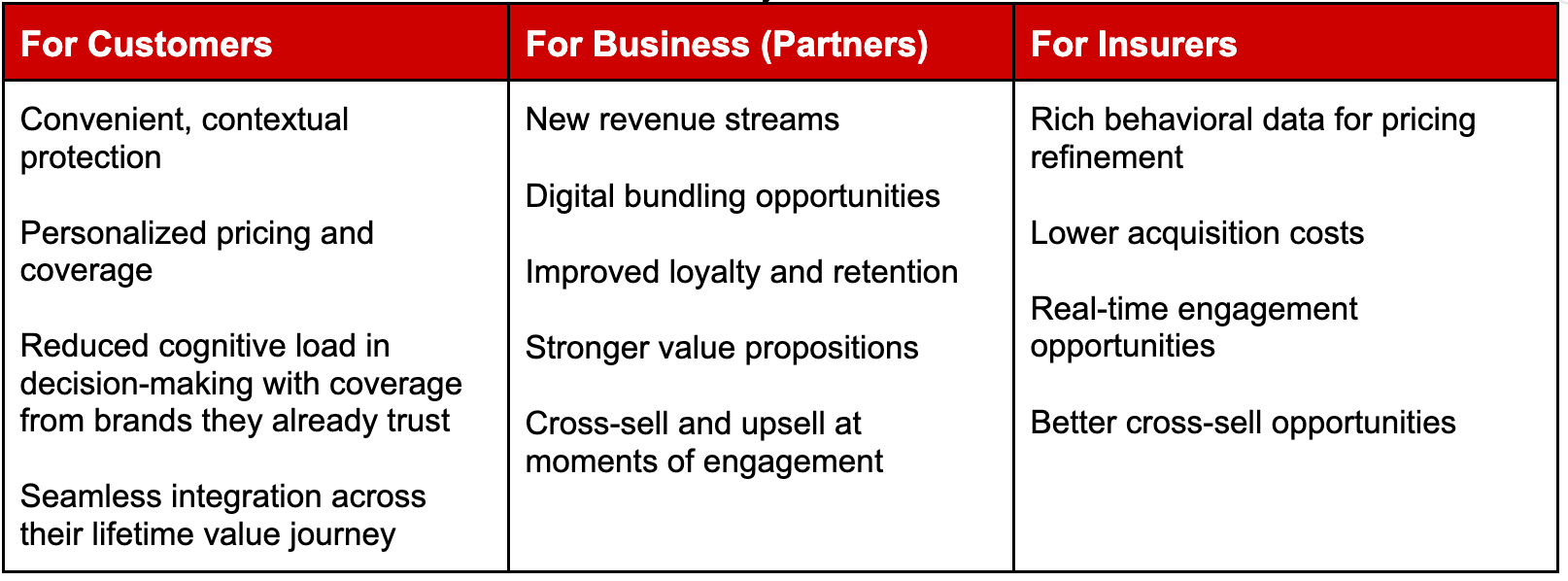

The Value Equation: Customer, Business, Insurer

Embedded models create value across the ecosystem. Consider some examples from different insurer types:

Consider some examples from different insurer types:

Life: Purchasing life insurance before a risky expedition or at the airport before a flight. With embedded insurance, life insurance companies can offer personalized coverage that better aligns with each consumer's unique circumstances. When one person in a family is more prone to illness than others, she can meet the deductible threshold when the family doesn’t meet it yet.

P&C: Automotive finance provider at the car dealership who is also licensed to sell insurance, car rental insurance that’s sold at the counter, or extended warranty offered when purchasing appliances. As per Weiss, actuaries are leveraging driving behavioral data to study variance in risk among customer segments to not only avoid adverse selection, but also to actively pursue

a more profitable portfolio of insured risks using telematics.

Cyber: Insurance for protection against ransomware attacks - a digital wallet user, while performing a high-value transaction, can be provided with cyber insurance coverage at the point of checkout.

Insurance that activates automatically, prices dynamically, and learns continuously from behavior requires more than APIs. It requires a real-time, governed data foundation.

A Real-World Example: Automotive Insurance

In this blog we’ll use the automotive industry to show how embedded insurance levels up. What if insurance pricing and coverage could adapt as fast as the trip itself?

This is where a real-time, governed data foundation drives value from edge to actionable insight and where embedded insurance and UBI insurance naturally converge as telematics devices create behavioral data used for pricing.

Drivers with safe driving habits and lower mileage should logically pay lower premiums. Telematics devices and smartphone apps now generate continuous streams of trip data including speed patterns, braking behavior, distance traveled, and driving conditions. Some insurers are going further - combining telematics with real time weather APIs to adjust risk dynamically based on environmental factors like active storms, severe weather alerts, flood zones, etc. for better insights. For example, alert a driver of a storm approaching resulting in proactive claim prevention.

Consider how a connected-vehicle insurer could combine geospatial, behavioral, and environmental data to derive deeper insights; Coverage is embedded directly into the vehicle purchase or app onboarding flow, so the customer receives a quote and activates a policy at the moment of vehicle delivery.

Pricing is usage-based, adjusting continuously using sensor data across multiple dimensions

- Driving behavior - harsh braking frequency, following distance, acceleration patterns

- Location patterns - frequency of driving or parking in higher-theft or higher-risk areas. Insuretechs like TNEDICCA provide ‘road risk intelligence’ to improve road safety through better use of crash location data and analytics.

- Environmental conditions - real-time weather signals that affect driving behavior metrics, such as active storm alerts or flood zone proximity

Risk scores update on each completed trip, and premiums adjust dynamically over time based on accumulated behavioral history.

Achieving this level of responsiveness requires real-time data triangulation across multiple sources. This is where a modern data architecture becomes essential.

The agentic AI playbook for the enterprise

Shared Data Foundation Across Personas

A real-time governed data foundation does more than modernize infrastructure. It transforms how different roles across the insurance organization make decisions and create value. While each persona uses the data differently, they all rely on the same governed data foundation.

- Underwriters refine pricing models.

- Product managers design adaptive coverage.

- Marketing teams deliver personalized engagement.

Because these teams operate on a unified platform like Databricks, they can collaborate using the same trusted datasets without duplication or silos. This shared intelligence layer is what enables insurance to evolve from static products to continuously adaptive protection.

The Underwriter: From Historical Risk to Behavioral Risk

Traditionally, underwriters rely on historical data, static rating factors, and periodic policy reviews to assess risk. This often means pricing decisions are based on incomplete or outdated information. With behavioral and contextual data flowing through the Lakehouse, underwriters gain a continuously updated view of risk along with the additional revenue flow.

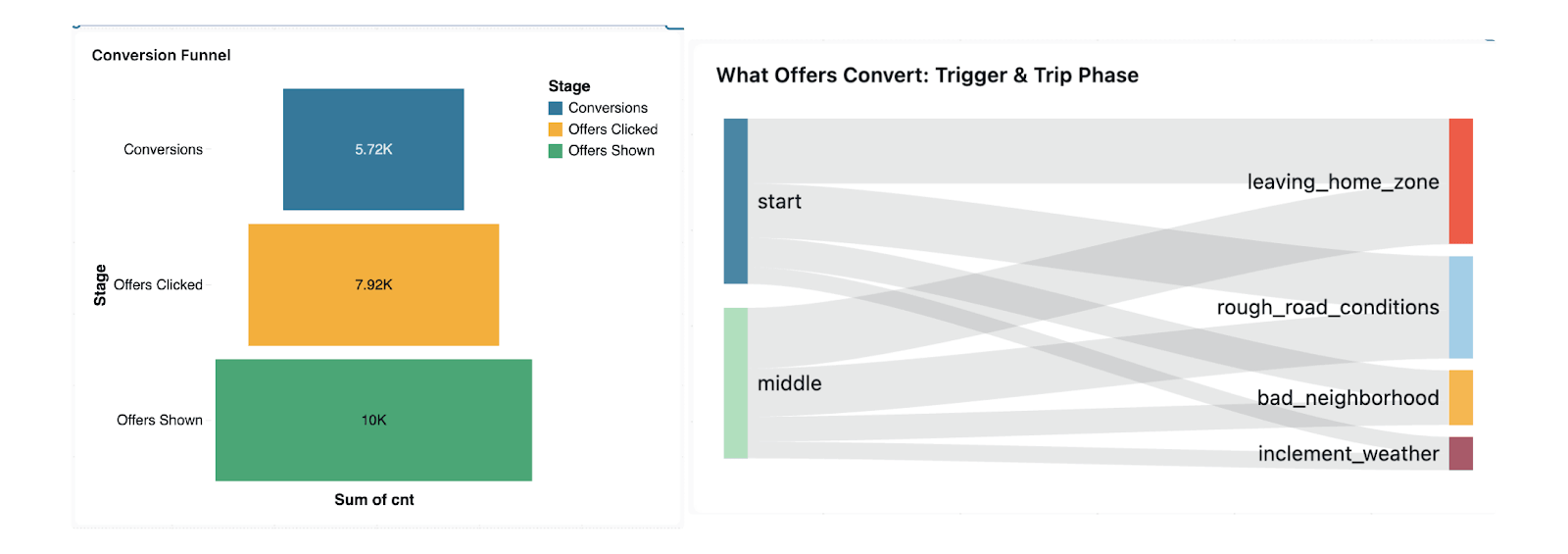

For example, in usage-based auto insurance, an underwriter can analyze aggregated driving behaviors such as harsh braking patterns, night driving frequency, or exposure to high-risk zones either on dashboard or by asking questions in natural language using Genie. These insights help refine underwriting guidelines and pricing models in near real-time.

Instead of relying solely on retrospective claims data, underwriters can incorporate live behavioral signals to improve pricing accuracy and reduce adverse selection. The result is more precise risk segmentation and more competitive products.

The Product Manager: Designing Adaptive Insurance Products

Product managers traditionally launch insurance products that remain fixed for long periods, often requiring months of regulatory filings, IT changes, and operational coordination.

With a unified data and AI platform, product teams can design dynamic, usage-based insurance products that respond to real-world behavior.

Consider an automotive product manager launching a “trip-based risk protection” feature. By leveraging real-time telemetry and geospatial data, the product can automatically adjust pricing or recommend temporary coverage when drivers enter higher-risk environments or face severe weather conditions.

Product managers can test new offerings, evaluate behavioral responses, and refine coverage triggers using live operational data rather than waiting for annual renewal cycles. This shortens product innovation cycles from quarters to weeks.

The Marketing Leader: Personalization at the Moment of Need

Marketing teams in insurance often struggle with limited behavioral insight and delayed campaign feedback. With real-time data, they can now analyze how drivers interact with embedded insurance offers across digital channels and understand which contextual triggers drive engagement. For example, they can correlate telematics device registrations with policy adoption across different geographies or identify which customer segments respond most strongly to usage-based pricing incentives.

Instead of broad campaigns, marketing teams can deliver contextual offers at the moment of need such as suggesting trip protection when a user books travel or offering temporary cyber coverage when a customer initiates a high-value digital transaction. Campaign effectiveness can be measured in near real-time, allowing teams to adjust messaging and targeting strategies dynamically.

How is it built on Databricks

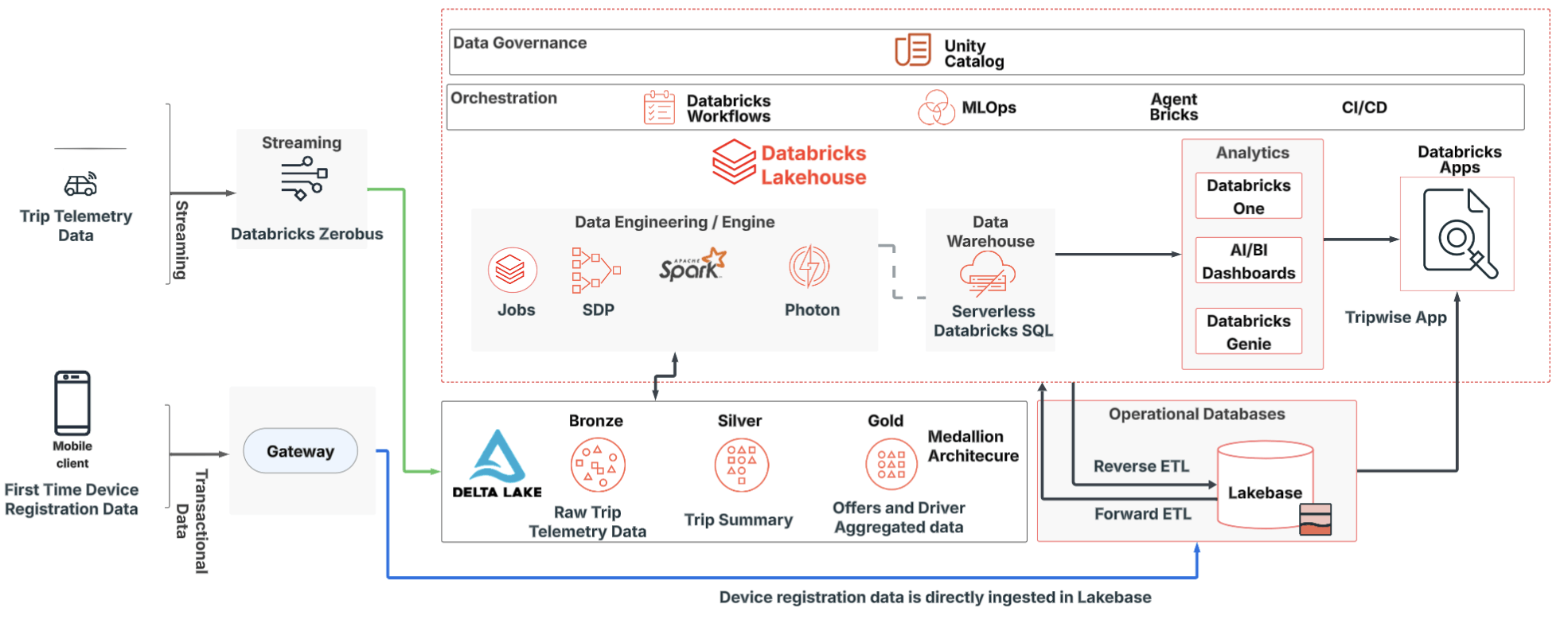

Today, many insurers struggle with fragmented device data, latency between risk signals and pricing, inflexible data pipelines, governance and explainability challenges. A modern Lakehouse architecture addresses these constraints by unifying data engineering, analytics, AI, and governance.

Device Onboarding & Trust: First-Time Registration

Every connected device establishes a verified identity, an ownership validation and a policy eligibility context. This foundation supports underwriting accuracy, fraud detection, and compliance from the start. Devices register once via a secure gateway after which the various trips are monitored in real time. Drivers typically get a small discount for using the telematics device or app and if their driving record is good, they are further rewarded by a discount to their premium.

This realtime data helps marketing teams determine the effectiveness of their campaigns by correlating device registration to driver policies in different geographies and adjusting campaign ads for better targeting.

Streaming Trip Data aka Risk Signals at Scale: Continuous

Devices continuously emit trip telemetry events that can be directly ingested by Zerobus directly to the Lakehouse, eliminating the need for additional hops via message buses and also decouples ingestion from analytics. Furthermore, it enables burst handling, real-time processing & replayability for audit and re-rating.

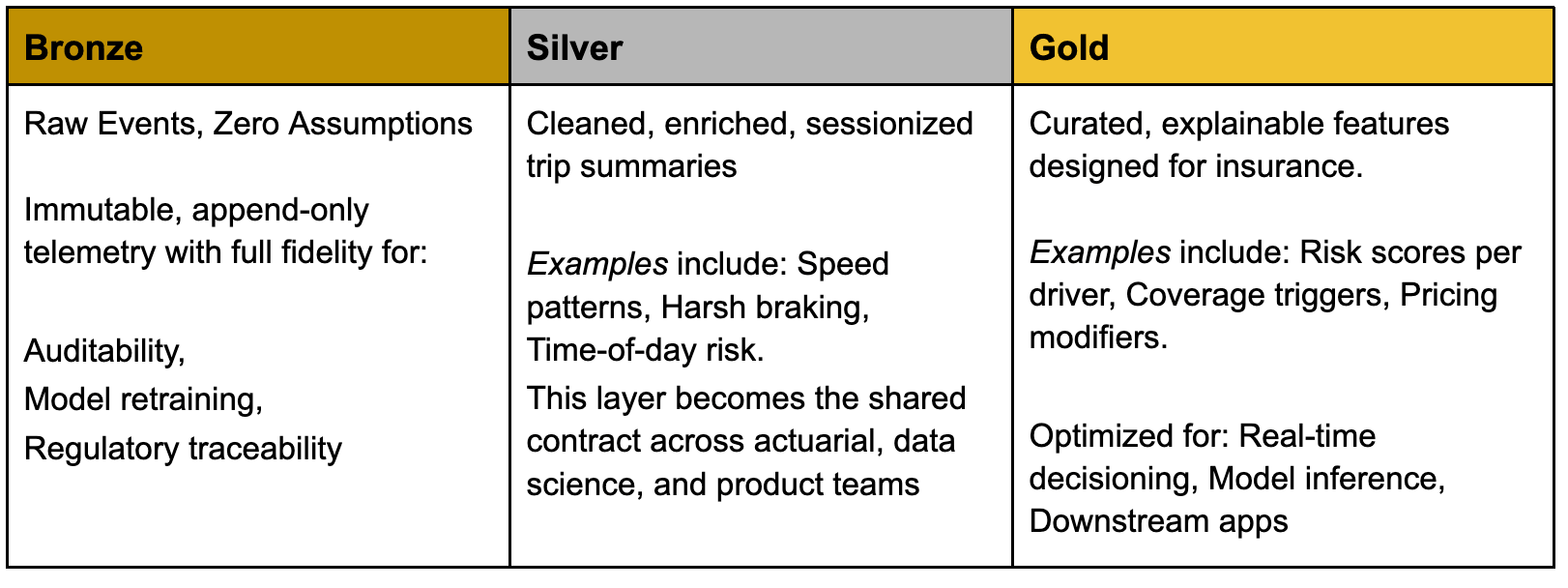

The Lakehouse in Action: From Raw Events to Insurance Decisions

A governed Medallion architecture translates telemetry into actionable insurance intelligence. Turning Data into Insurance Products

Turning Data into Insurance Products

Once curated in the Lakehouse, selected features can be operationalized into transactional systems to power insurance applications. Databricks enables insurers to build real-time insurance products by combining analytics, AI, and operational capabilities on a unified platform. For example:

- Lakebase provides low-latency access to curated features for pricing engines, policy systems, and partner APIs.

- Databricks One enables business users to access governed dashboards, natural language insights, and embedded analytics.

This architecture allows multiple teams - actuarial, underwriting, marketing, and product to work from the same trusted data foundation without duplication.

Governance: Trust as a Design Principle

As embedded insurance becomes more dynamic, regulatory scrutiny increases. Strong governance ensures insurers can innovate while maintaining transparency and compliance. Capabilities such as Unity Catalog enable:

- Fine-grained access controls across data layers

- Lineage tracking from device data to pricing decisions

- Model explainability tied back to source events

- Comprehensive audit trails for regulators

When governance is built into the architecture, trust becomes a competitive advantage rather than a constraint.

From Embedded Insurance to Autonomous Insurance

Embedded insurance definitely simplifies access to protection, whereas autonomous insurance takes the next step. In this future, model policies adjust dynamically in response to real-time risk signals. Claims, behavioral data, and pricing continuously inform each other. AI copilots assist underwriters and product managers in designing adaptive policies

The addition of Lakebase makes the Databricks Platform both the system of record and the system of intelligence.

Insurers that build this real-time data foundation today will move beyond contextual offers toward continuously adaptive protection, coverage that evolves alongside behavior, environment, and risk. This is what the Databricks platform uniquely enables! Static policies defined the past. Just-in-time insurance defines the present. Autonomous insurance will define the future.

Get the latest posts in your inbox

Subscribe to our blog and get the latest posts delivered to your inbox.