What is Open Banking?

Framework enabling secure sharing of financial data between banks and authorized third parties through standardized APIs, fostering innovation and choice

- Open banking is a framework where banks expose customer account data and payment capabilities to authorized third parties via secure APIs, with explicit customer consent, to encourage innovation and competition.

- Fintechs and banks use open banking to build services like account aggregation, personalized finance and new digital experiences while giving consumers more choice and control over their financial data.

- API reliability, privacy regulations and fragmented technical standards remain real barriers to open banking adoption, but platforms like Databricks Lakehouse for Financial Services help institutions address these challenges and share data securely at scale.

What is Open Banking?

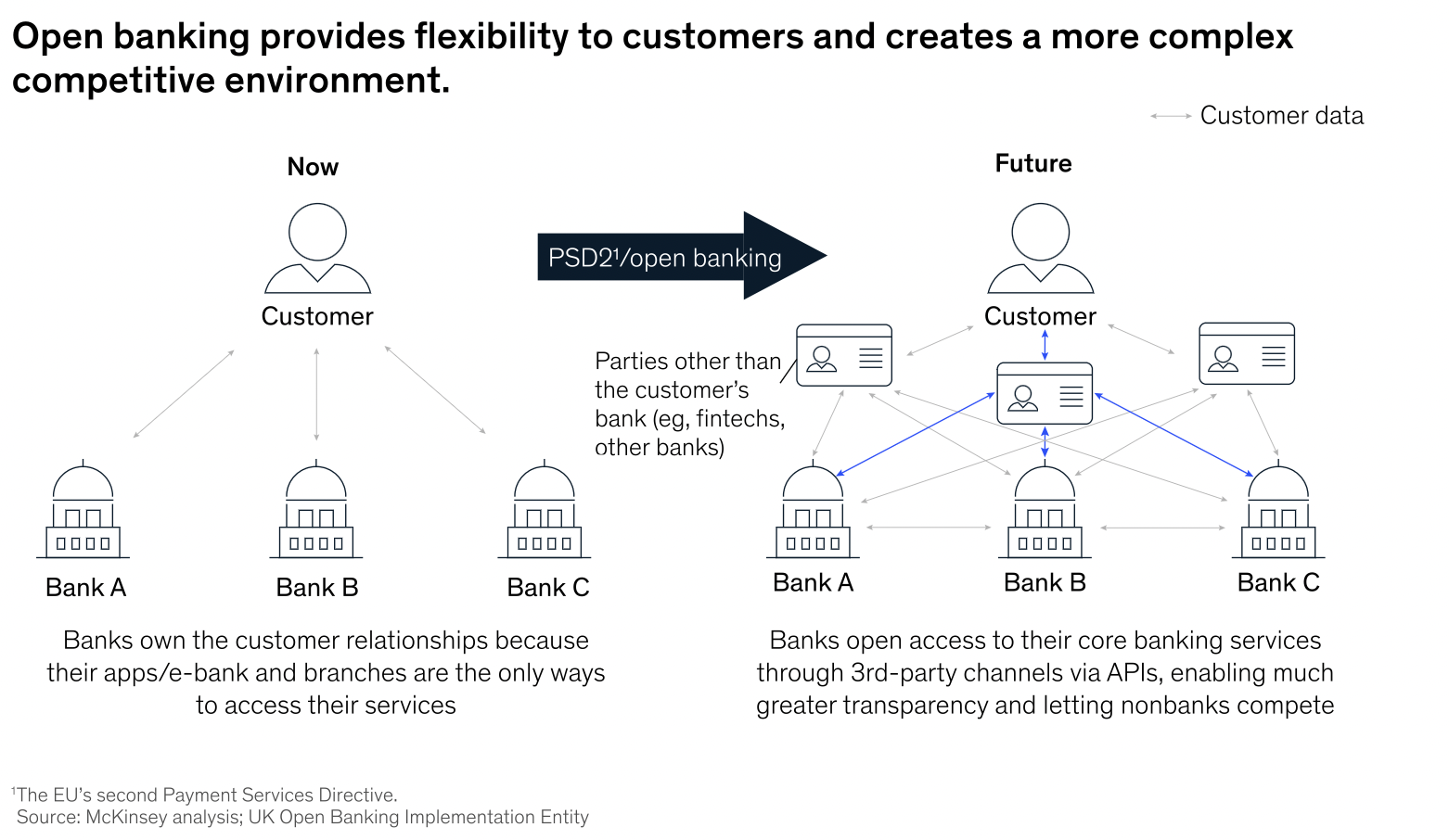

Open banking is a secure way to provide access to consumers' financial data, all contingent on customer consent.² Driven by regulatory, technology, and competitive dynamics, Open Banking calls for the democratization of customer data to non-bank third parties, consumers, etc. The innovation is both evolving the industry toward hyper-relevant, platform-based distribution and giving banks a rich opportunity to expand their ecosystems and extend their reach into new markets. With open banking, more financial service institutions (FSIs) expand access to customer data through application programming interfaces (APIs) and other data sharing models.

A wave of change is coming as Open Banking initiatives and regulations mature and enable the creation of the open data economy. One early indication is the rapid growth of third-party providers (TPPs) in Europe, which is at the forefront of the Open Banking paradigm. There, TPPs have grown from around 100 to more than 450 in under two years, and their focus has expanded from payments and transactional retail banking to encompass the entire financial value chain.

- 29% of banks' traditional retail products-based revenue streams are at risk.

- 55% boost to banking revenue expected by 2020 from new opportunities created by open API-enabled services.

Regulations on Open Banking have been vastly different between Europe and the U.S. As a result, Open Banking adoption in Europe has been largely regulatory-driven (this regulatory initiative is called PSD2) while in the US, open banking has and will likely continue to be market-driven.

|

86% |

8 out of 10 |

94% |

$9.9Bn |

|

of financial institutions recognize the value of Open Banking data |

financial institutions are adopting or plan to adopt Open Banking |

of FinTech companies have considered how Open Banking can enhance current services |

estimated total Open Banking sector revenues by 2022 |

Source: "Open Banking: Rearchitecting the Financial Landscape", FT Partners Research, March 2021; and OpenBanking.org, "Facts and Statistics"

What is the history of Open Banking?

Starting in the mid 2000s, regulations in Europe such as Payment Services Directive 1 (PSD1) was implemented to regulate and harmonize payments within Europe and assuage concerns surrounding security, data privacy and speed. PSD2 was drafted in 2013 and launched in 2018 to promote further interoperability between financial institutions and third parties. While PSD2 requires banks to open up their data, Open Banking Directive is a UK-specific initiative that requires banks to open up their data in a secure and standardized format in order to improve security as well as ease of use. This data includes customer financial data and transactions and is shared with third party providers only with the user's consent. While Open Banking began in the UK, it has spread to a number of countries in Asia and the United States.

Why is Open Banking important?

Open banking is more than a compliance exercise; it is an opportunity to enhance the customer experience. Heightened consumer expectations are driving banks to build open APIs – 67% of financial customers say they would share more data with banks in return for more benefits.3 Open banking allows banks to offer personalized finance (refer to Glossary: Personalized Finance) with open APIs or through banking-as-a-service (BaaS) platforms. For customers, open banking provides greater flexibility in how their money is managed allowing, for instance, better visibility of accounts and more convenient access to payments.

The value of Open Banking will initiate mostly in retail channels. Strategic partnerships within larger, mutually beneficial ecosystems will position banks to be visible and present to sell their offers whenever and wherever there's an opportunity. Banks can also provide developers with portals and sandboxes to build and test applications; following authorization, third party applications that securely access financial data can be offered to consumers. Because of this, a greater number of companies are able to compete in the financial services landscape, which should result in greater competition and rapid innovation in the market.

What are the challenges with Open Banking integrations?4

API performance and reliability. While developers can create public APIs to enable open banking, there's no guarantee the APIs will work reliably, especially across the various third-party applications and end-user configurations that they need to support. Testing third-party APIs is more important than ever.

Consumer worries. Consumer hesitancy towards open banking can be attributed to privacy and security concerns around sharing their transactional data. It is perceived as one of the most sensitive forms of information, and as a result, the friction around the privacy and security of open banking is one of the most significant barriers.

Lack of standardized compliance standards. Developers must contend with varying global compliance rules when creating open banking applications. This means there are no universal technical standards that define exactly how open banking integrations should work or how they can be used.

The agentic AI playbook for the enterprise

How does Databricks help financial institutions with Open Banking standards and implementation?

Lakehouse for Financial Services supports real-time analytics, business intelligence, and AI capabilities on all data types through a secure, multi-cloud environment. Specific solutions included for important financial use cases like open banking, compliance and regulatory reporting, post-trade analysis, risk management, and fraud detection.

In addition, Databricks Lakehouse has two sets of integration.

First, Databricks Delta Sharing empowers standardized, real-time data sharing with leading financial data providers like Nasdaq, FactSet and Intercontinental Exchange, making it easier to consume, share and monetize data through the platform. Second, it is also integrated with Legend, a cornerstone project of FINOS — the Fintech Open Source Foundation and a financial sector project of The Linux Foundation — to create an open ecosystem based on common standards for financial data throughout the entire banking ecosystem.

The potential benefits of open banking are substantial: improved customer experience, new revenue streams, and a sustainable service model for traditionally underserved markets, according to Mckinsey.5 Banks that do not build open APIs risk being left behind as consumers continue to shift to digital payments and banking applications.

What are the benefits of leveraging Databricks for open banking/open finance?

Lakehouse for Financial Services enables banks and open banking aggregators to address the challenge of merchant classification to enrich card transaction data with contextual information and gain further insights on transaction behaviors. With Lakehouse, FSs are able to unify data and AI on an open and collaborative platform to deliver personalized customer experiences, minimize risk, and accelerate innovation. The Lakehouse platform is:

Secure. PCI-DSS compliance for card transaction data and personal information

Scalable. Ability to process billions of card transaction data categorized for millions of consumers and merchants

Collaborative. Combining ML models and domain expertise to learn spending behaviors that drive segmentation.

2 www.openbank.org/customers/what-is-open-banking

4 https://www.rtinsights.com/4-challenges-for-open-banking-integration/

5 https://www.mckinsey.com/industries/financial-services/our-insights/data-sharing-and-open-banking

Additional Resources

Get the latest posts in your inbox

Subscribe to our blog and get the latest posts delivered to your inbox.